Is It the Right Time to Purchase Reverse Mortgage? Here’s What to Consider

Is It the Right Time to Purchase Reverse Mortgage? Here’s What to Consider

Blog Article

Empower Your Retired Life: The Smart Method to Acquisition a Reverse Mortgage

As retirement techniques, numerous individuals seek effective methods to improve their economic self-reliance and well-being. Among these strategies, a reverse home mortgage arises as a sensible choice for house owners aged 62 and older, enabling them to touch into their home equity without the need of monthly payments.

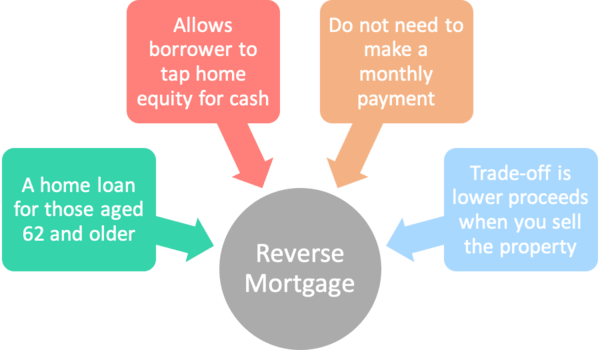

Recognizing Reverse Home Loans

Comprehending reverse home loans can be critical for home owners looking for monetary adaptability in retired life. A reverse home loan is a monetary item that allows qualified house owners, typically aged 62 and older, to convert a section of their home equity right into cash. Unlike conventional home loans, where customers make month-to-month payments to a lending institution, reverse home mortgages enable homeowners to get settlements or a lump sum while retaining possession of their building.

The quantity available via a reverse mortgage depends upon numerous variables, consisting of the house owner's age, the home's worth, and current rates of interest. Importantly, the funding does not have to be paid back till the property owner sells the home, relocates out, or dies.

It is crucial for prospective consumers to understand the effects of this monetary item, consisting of the effect on estate inheritance, tax obligation factors to consider, and recurring obligations related to building upkeep, taxes, and insurance. Furthermore, counseling sessions with certified experts are commonly called for to ensure that debtors completely understand the conditions of the car loan. In general, a thorough understanding of reverse home mortgages can encourage home owners to make educated choices regarding their financial future in retired life.

Advantages of a Reverse Home Mortgage

A reverse mortgage uses a number of compelling advantages for qualified property owners, especially those in retirement. This financial tool enables senior citizens to transform a section of their home equity right into money, supplying vital funds without the requirement for regular monthly home loan settlements. The cash obtained can be utilized for different objectives, such as covering clinical expenditures, making home renovations, or supplementing retirement income, hence enhancing general economic versatility.

One substantial advantage of a reverse home loan is that it does not need settlement till the property owner vacates, offers the home, or passes away - purchase reverse mortgage. This function allows senior citizens to preserve their way of living and meet unanticipated prices without the problem of regular monthly payments. In addition, the funds gotten are generally tax-free, enabling property owners to utilize their money without concern of tax obligation implications

In addition, a reverse home mortgage can offer assurance, understanding that it can act as a monetary safety and security web throughout tough times. Home owners likewise preserve possession of their homes, ensuring they can proceed residing in an acquainted environment. Eventually, a reverse home loan can be a critical funds, encouraging retired people to handle their financial resources efficiently while enjoying their gold years.

The Application Process

Browsing the application process for a reverse home loan is a vital step for property owners considering this monetary option. The initial stage involves assessing qualification, which normally calls for the property owner to be a minimum of 62 years old, own the residential or commercial property outright or have a low mortgage equilibrium, and inhabit the home as their primary house.

When eligibility is validated, house owners have to go through a counseling session with a HUD-approved therapist. This session guarantees that they fully recognize the ramifications of a reverse home mortgage, consisting of the obligations involved. purchase reverse mortgage. After finishing therapy, applicants can proceed to gather essential paperwork, including evidence of earnings, assets, and the home's worth

The next action requires sending an application to a loan provider, that will certainly assess the monetary and residential or commercial property credentials. An assessment of the home will certainly likewise be conducted to establish its market price. If accepted, the loan provider will certainly offer lending terms, which ought to be reviewed meticulously.

Upon acceptance, the closing procedure complies with, where last files are signed, and funds are disbursed. Recognizing each phase of this application procedure can significantly enhance the property owner's self-confidence and decision-making pertaining to reverse home mortgages.

Secret Considerations Prior To Buying

Getting a reverse home loan is a substantial financial choice that calls for cautious consideration of numerous crucial elements. First, understanding your qualification is vital. House owners must go to the very least 62 years old, and the home should be their primary home. Evaluating your economic requirements and goals is similarly important; establish whether a reverse mortgage aligns with your long-lasting plans.

Moreover, assess the effect on your present way of living. A reverse home loan can impact your qualification for sure federal government benefits, such as Medicaid. Lastly, look for specialist guidance. Consulting with a financial consultant or a housing therapist can provide important insights customized to your individual situations. By thoroughly reviewing these considerations, you can make an extra enlightened choice regarding whether have a peek at these guys a reverse home mortgage is the appropriate monetary method for your retired life.

Making the Most of Your Funds

Once you have protected a reverse home mortgage, efficiently taking care of the funds becomes a top priority. The adaptability of a reverse home loan allows property owners to make use of the funds in numerous means, however critical planning is necessary to optimize their advantages.

One crucial technique is to develop a spending plan that outlines your economic objectives and month-to-month expenditures. By determining essential costs such as healthcare, residential or commercial property tax obligations, and home upkeep, you can allot funds accordingly to guarantee long-lasting sustainability. Furthermore, take into consideration utilizing a part of the funds for financial investments that can create income or appreciate with time, such as dividend-paying supplies or shared funds.

Another important aspect is to keep a reserve. Reserving a book from your reverse mortgage can assist cover unanticipated expenses, providing comfort and financial security. Moreover, talk to a monetary expert to check out possible tax ramifications and just how to integrate reverse home loan funds into your general retirement approach.

Ultimately, sensible monitoring of reverse home mortgage funds can enhance your monetary safety and security, enabling you to appreciate your retired life years without the anxiety of monetary uncertainty. Cautious preparation and notified decision-making will certainly guarantee that your funds work properly for you.

Final Thought

Finally, a reverse mortgage presents a practical economic strategy for seniors seeking to boost their retired life experience. By converting home see this page equity into accessible funds, individuals can deal with essential costs and secure extra funds without incurring month-to-month payments. Cautious consideration of the linked terms and effects is vital to take full advantage of benefits. Ultimately, leveraging this economic tool can help with greater freedom and improve total lifestyle throughout retirement years.

Recognizing reverse mortgages can be important for homeowners seeking economic versatility in retirement. A reverse home loan is a financial item that permits eligible house owners, normally aged 62 and older, to transform a portion of their home equity right into money. Unlike typical home loans, where borrowers make monthly payments to a loan provider, reverse home loans enable home owners to get settlements or a lump amount while preserving possession of their residential or commercial property.

Generally, a complete understanding of reverse mortgages can equip property owners to make educated decisions regarding their monetary future in retirement.

Consult with a monetary advisor to explore feasible tax ramifications and how to incorporate reverse home mortgage funds into your general retirement method.

Report this page